Failed Home Inspection? Using a Reverse Mortgage for Critical Repairs

A failed inspection reveals expensive foundation, roof, or electrical repairs. A reverse mortgage can fund these critical repairs without selling your home or going into unsecured debt.

A home inspection reveals structural damage, a failing foundation, outdated electrical, or a roof nearing failure. The contractor's quote: $35,000–$80,000. Your retirement income can't accommodate a monthly loan payment. You're stuck between three bad options: ignore the problem and watch your home deteriorate, sell the home you want to stay in, or take on credit card debt at 19.99% interest. A reverse mortgage offers a fourth option.

When Home Inspections Reveal Hidden Costs

Many Ontario homes built in the 1960s–1980s are reaching the end of design life for critical systems:

Common expensive repairs:

- Roof replacement: $8,000–$15,000 (asphalt shingles last 15–25 years; if yours is 25+ years old, replacement is urgent)

- Foundation repair: $15,000–$50,000+ (settling, cracks, water intrusion; varies wildly by severity)

- Electrical system upgrade: $10,000–$25,000 (if your home has outdated or dangerous wiring; knob-and-tube requires replacement; aluminum wiring needs assessment)

- Plumbing replacement: $5,000–$25,000 (if galvanized pipes are corroded or asbestos is present)

- HVAC replacement: $12,000–$20,000 (covered separately in our heating/cooling guide)

- Window and door replacement: $8,000–$20,000 (if extensive single-pane windows or rotting frames)

- Chimney repair or removal: $3,000–$12,000 (if unsafe or needs rebuilding)

Why this matters: These are often safety issues. A failing roof doesn't just damage aesthetics—water intrusion leads to mold, structural rot, and health hazards. Outdated electrical can be a fire risk. A failing foundation compromises home stability.

Many homeowners can't ignore these issues without risking safety, health, or further deterioration that makes repairs exponentially more expensive.

The Cost of Delaying Repairs

One of the hidden costs of deferred maintenance is compound deterioration:

Example: The leaking roof

| Year | Issue | Cost | Cumulative Cost |

|---|---|---|---|

| Year 1 | Roof leaks identified | Ignore it—save money | $0 |

| Year 2 | Water infiltrates attic | Mold appears; smell detected | $1,500 (mold remediation) |

| Year 3 | Water seeps into walls | Drywall damaged; insulation saturated | $8,000 (wall repair, insulation replacement) |

| Year 4 | Structural framing rots | Support beam damaged | $25,000 (structural repair) |

| Year 5 | Full roof replacement needed | Plus structural repairs | $40,000+ |

By delaying a $10,000 roof repair by five years, you end up with a $40,000 problem. The "savings" of waiting have become a catastrophe.

Why a Reverse Mortgage Solves This Problem

When faced with urgent repairs, Ontario seniors typically have a few funding options:

| Option | Pros | Cons |

|---|---|---|

| Pay in cash from savings | No debt; immediate | Depletes emergency reserves |

| HELOC (Home Equity Line of Credit) | Funds available; lower rate than unsecured debt | Monthly payments strain fixed-income budget; requires good credit |

| Personal loan or credit card | Quick approval | 8–20% interest; adds monthly payment burden |

| Reverse mortgage | No monthly payments; funds available; reasonable interest rate | Interest compounds; reduces inheritance |

| Sell home and buy smaller | Solves debt problem; simplifies life | Loss of family home; moving costs; may regret relocation |

For most retirees on fixed incomes, a reverse mortgage is the best fit. Here's why:

Monthly budget impact:

- HELOC on $30,000 at 6.5%: $162.50/month interest (+ principal repayment)

- Credit card on $30,000 at 19.99%: ~$500/month minimum payment

- Reverse mortgage on $30,000 at 6.54%: $0/month payment, interest accrues

On a $3,500/month retirement income, a $162.50+ HELOC payment is significant. A reverse mortgage preserves monthly cash flow while repairs happen.

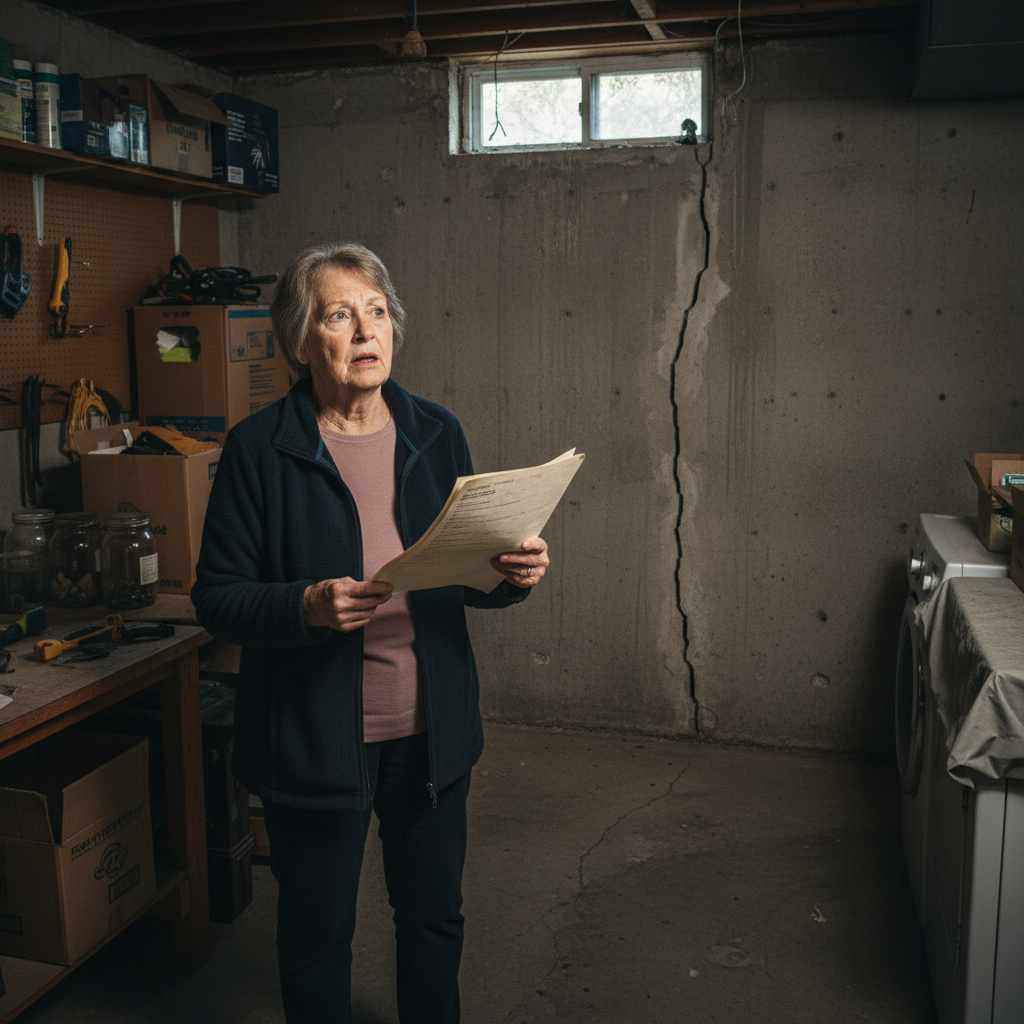

Real-World Example: Helen's Foundation Problem

Helen, 73, lived in a semi-detached in Scarborough that she'd owned since 1988. During a home inspection (she was considering downsizing), the inspector found a 25-foot crack in her foundation with signs of water infiltration in the basement.

Foundation engineer's assessment: $45,000 repair, needed within 18 months before winter freezing worsened the damage.

Helen's situation:

- CPP: $1,400/month

- Pension: $1,800/month

- Investment income: $300/month

- Total: $3,500/month

- Home value: $675,000

- Home equity (after existing $150,000 mortgage): $525,000

Options Helen considered:

-

Downsize: Sell for $675,000, buy a condo for $400,000, use $275,000 to eliminate existing mortgage and fund repairs, keep ~$185,000 as liquid reserve. Sounds good, but Helen loved her home of 35 years and wasn't ready to leave.

-

HELOC: Access $45,000 via HELOC at 6.5%. Monthly payment would be $244/month interest + principal repayment over 10 years (~$450/month total). Her monthly income wouldn't stretch.

-

Personal loan: Take a $45,000 unsecured personal loan at 8% over 10 years. Monthly payment: ~$580/month. Not feasible.

-

Reverse mortgage: Access $45,000 via reverse mortgage at 6.54%. No monthly payment. Balance grows to ~$62,000 over 10 years but she stays in her home debt-free monthly.

Helen's choice: Reverse mortgage.

She closed a reverse mortgage and accessed $45,000. Foundation repairs started within two months. She maintained her $3,500/month income without additional payments. In 10 years, if she sells, the foundation repair will have added far more value than $62,000 to her home. The reverse mortgage cost (compound interest) was offset by:

- Preventing further structural damage (saved $20,000+)

- Maintaining home value ($675,000 vs. $400,000 if she'd downsized)

- Preserving ability to stay in her home (priceless to Helen)

Planning Major Repairs with a Reverse Mortgage

If you've had a home inspection revealing major repairs:

Step 1: Get multiple contractor quotes

Don't accept the first estimate. Get 3 quotes for any repair over $10,000. Compare:

- Scope of work (are all quotes covering the same work?)

- Warranty (how long are they guaranteeing the repair?)

- Timeline (can you choose urgent vs. staged?)

- References (talk to previous customers)

Step 2: Prioritize by urgency and cost

| Priority | Examples |

|---|---|

| Urgent (do now) | Electrical hazards; roof leaks; structural damage |

| Important (do within 2 years) | HVAC replacement; outdated plumbing; foundation issues |

| Moderate (do within 5 years) | Windows; siding; aesthetic upgrades |

Step 3: Explore cost reduction

- Can repairs be staged? (Roof sections at a time instead of all at once)

- Are there government rebates for upgrades? (Heat pumps, energy-efficient windows, accessibility modifications)

- Can you do some work yourself or with volunteer help? (Painting, landscaping; not structural work)

Step 4: Model reverse mortgage cost vs. alternatives

Work with your reverse mortgage advisor to understand:

- How much you can borrow

- What the balance will grow to over time

- How this compares to HELOC, loans, or selling

Special Consideration: Critical Repairs for Aging in Place

If you plan to age in place, certain repairs become foundational:

- Safe electrical: For medical equipment (oxygen, dialysis), charging mobility aids, safety lighting

- Accessible bathroom: To prevent falls and enable independence

- Structural integrity: So your home doesn't become dangerous or uninhabitable

- Climate control: For health (especially if you have cardiac or respiratory conditions)

These repairs are investments in your independence and safety—not just home maintenance. A reverse mortgage for these repairs is particularly justified because it directly enables aging in place.

Questions for Your Contractor

When getting repair quotes:

- What would happen if we delay this repair? (Understand true urgency)

- Are there temporary solutions we could do now, permanent fixes later? (Staging)

- What warranty do you offer on parts and labour? (10-year is standard for major work)

- Can you provide references from other seniors you've worked with? (Verify reliability)

- Are there permit requirements? (Some major work needs city approval; understand timeline)

- What's included and not included in the quote? (Confirm scope)

Avoiding Contractor Scams

High-cost repairs attract predatory contractors. Protect yourself:

- Never hire a contractor who approaches you with unsolicited quotes

- Don't pay cash in advance; pay upon completion

- Get everything in writing

- Verify they're licensed and insured

- Check references directly (not just names they provide)

- If pressure is applied, walk away

After the Repair: Tracking Home Condition

Once major repairs are complete:

- Keep detailed records — document what was fixed, warranties, contractor contact info

- Annual maintenance — small preventive maintenance ($200–$500/year) prevents major repairs later

- Monitor your reverse mortgage balance — track how much interest has accrued

- Plan for future repairs — as you age, anticipate what else might need attention (HVAC at 15 years, roof at 25, etc.)

Should You Get a Pre-Emptive Home Inspection?

If your home is 25+ years old and you haven't had a recent inspection, should you get one before considering a reverse mortgage?

Pros of getting an inspection:

- Identifies hidden problems before they become catastrophic

- Helps you decide whether to stay in the home or move

- Allows you to plan and budget repairs strategically

Cons:

- Costs $400–$600

- May reveal problems you weren't ready to address

Recommendation: If you plan to stay in your home 10+ years, a $500 inspection is worthwhile. It provides clarity and allows strategic planning rather than reactive crisis management.

The Bottom Line

Home inspections that reveal expensive repairs feel like disasters. But they're actually important information that helps you make good decisions. A reverse mortgage allows you to address critical repairs while maintaining your independence and monthly cash flow.

Rather than panic-selling your home to avoid a $45,000 repair, you can stay, fix the problem, and age in place safely and comfortably.

If you've discovered home repairs you can't easily afford, explore how a reverse mortgage could help you fund these urgent investments while keeping your home.

Ready to Learn More?

Get the free Ontario Reverse Mortgage Guide and find out exactly how much you could unlock from your home.

Get My Free Guide →Related Articles

Reverse Mortgage as Bridge Financing: Funding the Gap While Your Home Sells

Use a reverse mortgage as bridge financing to cover living expenses while waiting for your current home to sell. Ontario strategy guide for 2026.

Read →Reverse Mortgage and Deferred Home Maintenance: Catching Up on Repairs

Use a reverse mortgage to fund essential home repairs and maintenance you've deferred—preventing costly damage and maintaining aging in place.

Read →Reverse Mortgage for Home Renovations: Aging in Place Guide for Ontario Seniors

Learn how to use a reverse mortgage to fund home renovations and modifications that let you age in place safely and comfortably in your Ontario home. Includes cost examples and step-by-step process.

Read →